》Check SMM Copper Quotes, Data, and Market Analysis

》Click to View Historical Spot Copper Price Trends on SMM

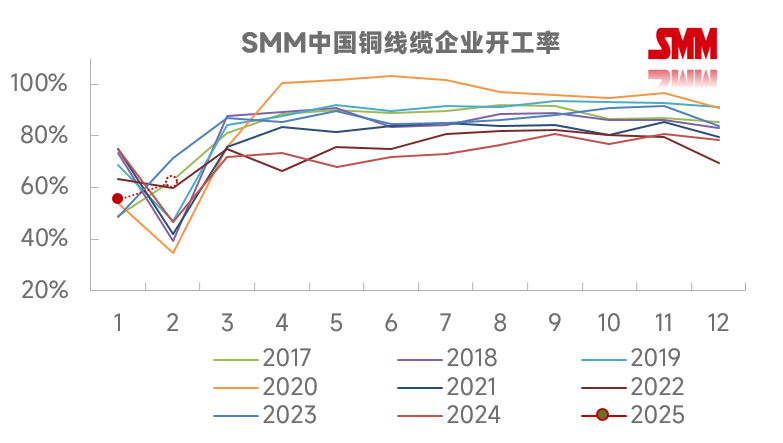

According to SMM, the operating rate of copper wire and cable enterprises in January was 55.25%, down 23.1 percentage points MoM, down 19.85 percentage points YoY, but 8.5 percentage points higher compared to February last year (Chinese New Year month), and 16.11 percentage points lower than the expected operating rate. Among them, the operating rate of large enterprises was 58.84%, medium-sized enterprises 45.23%, and small enterprises 28.87%.

Data Source: SMM

The significant decline in the operating rate of copper wire and cable enterprises in January, which was far below expectations, was mainly due to the following reasons:

- Most enterprises suspended operations due to the Chinese New Year break, with only a few production lines maintained by some enterprises;

- The continuous upward shift in copper price centers in January suppressed customer purchasing enthusiasm; market demand was moderate in early January but gradually weakened thereafter. In particular, demand for medium- and low-voltage orders for construction and infrastructure was notably weak, while power generation orders also gradually softened. Only power grid orders remained relatively stable;

- Some enterprises in the sample accelerated production in late December 2024 to boost output value, thereby depleting January's production in advance.

In terms of inventory, the raw material inventory of SMM copper wire and cable samples in January recorded 42,350 mt, down 1,242 mt MoM. The pre-holiday inventory was almost entirely consumed, with the raw material inventory/output ratio at 25.25%, up 6.92 percentage points. Meanwhile, finished product inventories recorded 46,560 mt, up 1,590 mt MoM, with the finished product inventory/output ratio at 27.76%, up 8.85 percentage points MoM. Post-holiday, enterprises resumed production slowly, focusing on consuming finished product inventories.

SMM expects the operating rate of copper wire and cable enterprises in February to increase by 6.79 percentage points to 62.04%, up 15.29 percentage points YoY (as February 10, 2024, marked the Chinese New Year, resulting in more holiday time in February). Most enterprises in the industry resumed work on February 5 (the eighth day of the lunar calendar), but some workers will not fully return until the Lantern Festival (February 14). Downstream customers are also in the process of recovery. In the first half of February, the increase in new orders was limited, and enterprises mainly relied on previous orders on hand to maintain production. The sharp rise in copper prices after the holiday intensified downstream customers' wait-and-see sentiment, with only a few channel customers reportedly placing orders amid a "rush to buy" scenario, further delaying the release of new orders in the market. Copper wire and cable enterprises generally believe that operating rates will not return to normal levels until March. By industry, power grid orders, which were tendered by the end of 2024, are expected to materialize in March. New orders for new energy power generation are gradually recovering, while orders for construction and infrastructure remain weak.